Why Mid-Year 2026 Is the Right Readiness Checkpoint

Six months of current data — giving trends, budget performance, board decisions, and project progress — makes mid-year a practical time to understand whether the church is prepared to move forward responsibly.

What lenders generally evaluate

Church lenders generally evaluate giving consistency and trajectory, cash available for debt service, reserve stability, existing debt obligations, and board alignment. Construction and renovation projects also require scope definition and cost validation.

What happens when preparation begins too late

Incomplete documentation, undefined project scope, or unresolved board questions may require revised projections, additional approvals, or a pause while the church clarifies its position.

The value of a readiness conversation

A church does not need every answer before speaking with a church-financing specialist. The first conversation can clarify its current position, identify material gaps, and determine whether the next step is an application or additional preparation.

About This Brief

This qualitative lender-insight brief draws on recurring church-finance questions and professional observations from Griffin Church Loans' experience since 1999. It is an educational readiness resource, not a statistical analysis of Griffin's complete loan portfolio or a statement of universal underwriting requirements.

- Publication date: June 2026

- Prepared by: Griffin Church Loans

- Founder perspective: John Berardino, Founder and President

- Scope: Construction, renovation, property purchase, and refinancing readiness

What Church Leaders Should Review

Mid-year readiness is not about predicting the lending market. It is about using current financial and organizational information to determine whether the church is prepared to move forward responsibly.

Financial

- YTD giving vs. prior year

- Actual spending vs. budget

- Reserve movement

- Existing debt obligations

Governance

- Board understanding

- Decision authority

- Payment clarity

- Leadership alignment

Project

- Defined scope

- Current estimates

- Contingency assumptions

- Third-party requirements

Timing

- Date funds are needed

- Document preparation

- Approval schedule

- Appraisal and title work

What It Means to Be Ready for a Church Loan

Almost every early church-finance conversation begins with some version of the same question: Are we ready? The useful answer is structured rather than binary. A church may be financially capable but not project-ready. It may have a defined project but incomplete financial records. It may have adequate cash flow but insufficient board alignment.

Who this brief is for

Pastors, trustees, church board members, treasurers, finance committee leaders, and other authorized decision-makers considering a property purchase, refinancing, renovation, expansion, or construction project.

Why church-specific context matters

Giving patterns, ministry expenses, governance structures, leadership stability, reserves, property use, and congregational support all affect how a church's financial position is understood.

What readiness does not mean

- Every question has already been resolved.

- Approval or specific loan terms are guaranteed.

- The church must delay an initial conversation until every document is perfect.

- It does mean the church understands its current position and is prepared to address material gaps.

Personal-Guarantee Requirements

Pastors and board members often assume that individuals will need to place personal assets behind a church loan. Some general commercial lenders require personal guarantees under their standard policies or for particular transaction structures. Other church-finance programs may focus primarily on the organizational strength of the church.

What a church-focused evaluation generally considers

- Giving history and trajectory

- Operating results and cash available for debt service

- Reserve stability and liquidity

- Existing debt obligations

- Governance and board authorization

- Leadership stability

- Property and collateral

- Transaction structure

Church leaders should ask about guarantee expectations at the beginning of the process. The absence of a personal guarantee does not remove the need for strong organizational documentation, sustainable repayment capacity, appropriate collateral, or approvals.

How to Get a Church Loan: Avoid Personal Guarantees and Fund Your Vision

Giving Trends and Financial Documentation

A church reporting $700,000, $750,000, and $800,000 over three consecutive years presents a different trajectory from one reporting $900,000, $850,000, and $800,000, even though both end at the same annual total.

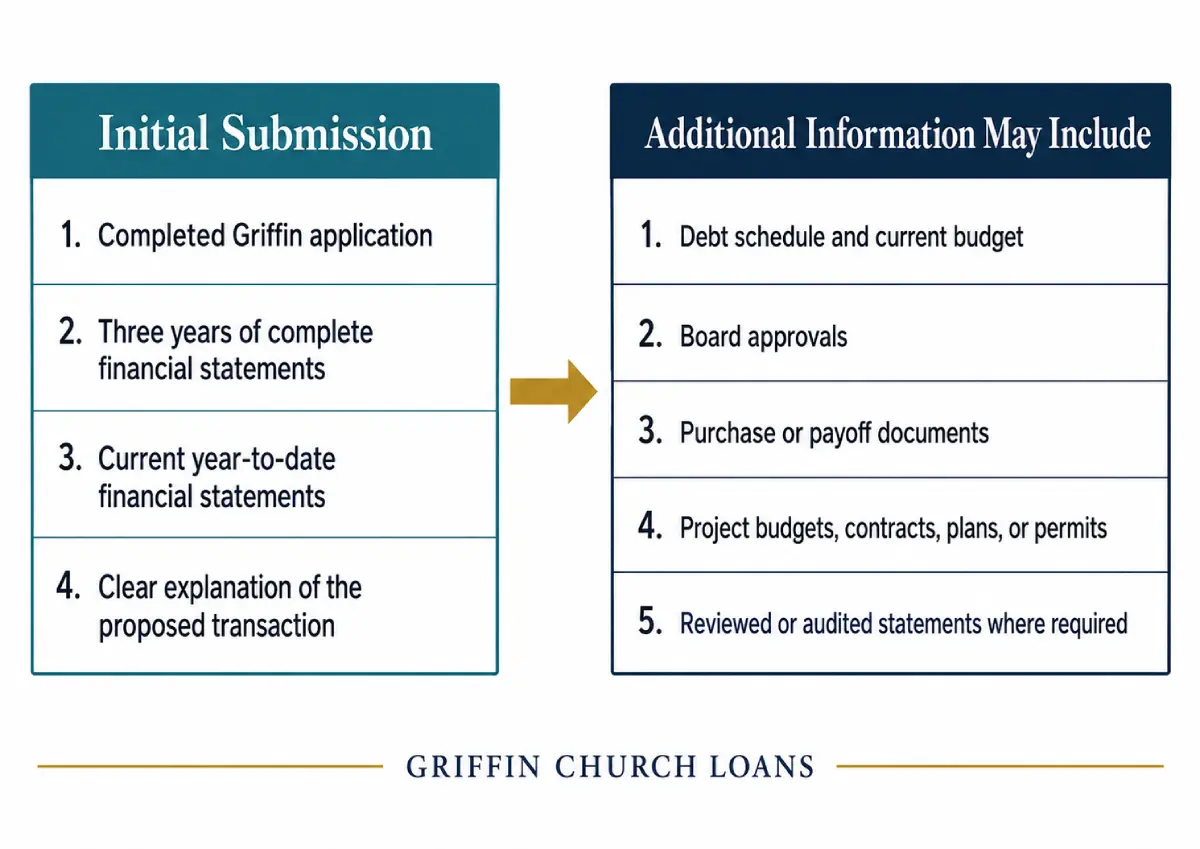

Document Flow Infographic

Document Flow Infographic

Typical initial submission

- Completed Griffin application

- Three years of complete financial statements

- Current YTD financial statements

- Clear explanation of the proposed transaction

Additional information may include

- Debt schedule and current budget

- Board approvals

- Purchase or payoff documents

- Project budgets, contracts, plans, or permits

- Reviewed or audited statements where required

Documentation issues that can slow review

- Statements that do not reconcile

- Missing months or incomplete periods

- Different accounting methods without explanation

- Restricted funds presented as freely available cash

- Omitted debt obligations

- Unexplained material budget variances

Board Alignment and Governance

A formal board resolution is commonly required. The lender may need to understand who has authority to borrow, whether the proposal is consistent with the church's governing documents, and whether the board reviewed the financial implications — not only the ministry objective.

Governance signals

- Clear authority under governing documents

- Defined board, trustee, or congregational process

- Leadership stability

- Access to current financial information

- Formal resolution reflecting the financing purpose

Board preparation

- Present giving, reserves, debt, and operating results together

- Review the proposed monthly payment against the budget

- Separate project cost, requested financing, available cash, and debt service

- Confirm the approval process required by governing documents

Additional guidance: Church Financing Guidelines for Church Boards and Financial Literacy for Nonprofit Boards.

Timing and Planning

A compressed timeline does not eliminate the steps required to evaluate and close a church loan. It reduces the time available to complete them accurately.

How early should planning begin?

Churches should generally begin several months before funds are needed. No universal closing timeline applies; the required period depends on the transaction and the readiness of the church's file.

Pre-application milestones

- Property purchase: identified property, purchase agreement or letter of intent, down-payment source, financial records, and approval path.

- Refinancing: current loan statement, maturity, payoff details, financing objective, and expected-benefit comparison.

- Renovation: defined scope, current estimates, approved budget, required equity source, and current statements.

- Construction: establish a preliminary borrowing range before committing significant funds to plans, contractors, or third parties.

Reserves and Repayment Capacity

The lender needs to understand whether the payment fits after normal operating expenses, whether existing debt remains manageable, and whether the church has sufficient liquidity to absorb a temporary disruption.

What lenders may consider

- Available operating cash and unrestricted liquidity

- Stability and source of reserves

- Recent reserve movement

- Restricted or donor-limited funds

- Capital-campaign proceeds

- Relationship between reserves and debt service

Questions for the finance committee

- What is the monthly and annual debt service?

- How does it compare with available cash flow?

- What happens if giving falls below budget?

- Which reserves are truly available?

- What other obligations must be carried?

- Does the payment remain sustainable after contingencies?

How repayment capacity is generally evaluated

Debt-service coverage generally compares cash available for debt service with required annual debt payments. The precise calculation, adjustments, and minimum expectations vary by lender, program, and transaction.

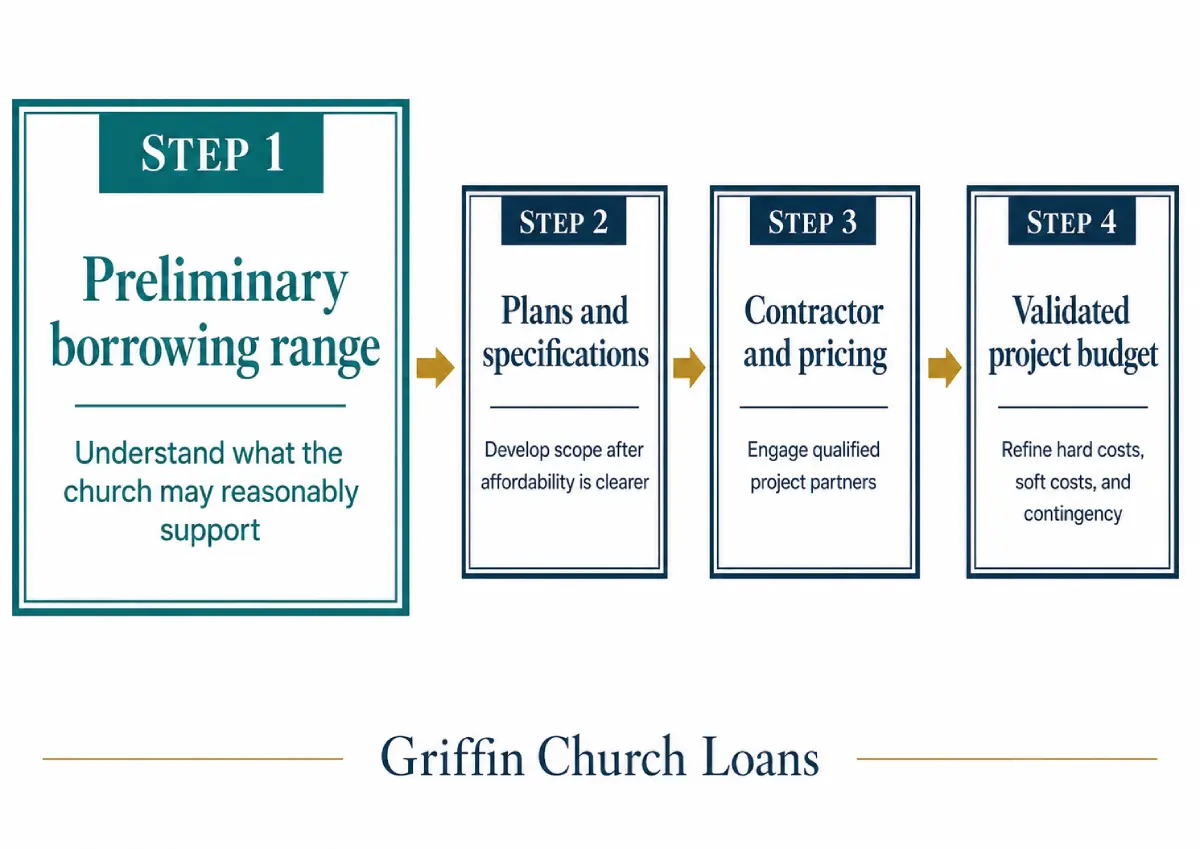

Construction-Loan Readiness

A construction concept is an appropriate beginning, but it is not yet an underwritable project. The church and financing team need enough detail to understand what will be built, what it is expected to cost, and how the church will carry the obligation during and after construction.

Construction Readiness Sequence Infographic

Construction Readiness Sequence Infographic

Recommended construction-readiness package

- Developed plans, specifications, or a clearly defined scope

- Qualified general contractor under contract or letter of intent

- Complete budget including hard costs, soft costs, site work, fees, and furnishings

- Project-specific contingency

- Construction schedule

- Board authorization

- Understanding of draw, inspection, lien-waiver, and disbursement processes

- Plan for permanent financing or conversion, where applicable

Recurring construction-readiness gaps

- A church may begin a financing conversation while the project is conceptual; the risk is spending substantially before establishing a realistic borrowing range.

- Early estimates that exclude site work, design, permits, contingency, or furnishings

- Scope changes after the financing amount has been evaluated

- Assuming every project cost can be financed without confirming program requirements

- Board approval covering the vision but not the validated budget and obligation

How Does a Church Know It Is Ready to Apply?

Readiness is not perfection. It is the point at which the church and financing team can evaluate the transaction using complete enough information to reach responsible decisions.

- Three years of financial statements are complete and consistent.

- Current YTD giving and operating results are available and understood.

- Reserve balances are documented and restricted funds are distinguished.

- Existing debt and material obligations are fully documented.

- The board has reviewed the purpose, cost, requested amount, and payment.

- The project scope and budget are sufficiently defined.

- The proposed payment has been compared with the operating budget and cash flow.

- The schedule allows time for underwriting, approvals, third-party work, and closing.

The most important affordability question

Has the finance committee reviewed the proposed monthly payment against the church's actual operating budget and concluded that the church can sustain it with a reasonable margin?

What to do when the church is not yet ready

Many gaps can be addressed through clearer documentation, board alignment, project development, or additional preparation time. An initial conversation with Griffin can occur before every issue is resolved.

Church Loan Readiness Scorecard

Mark the current status of each area. The tool is a discussion aid — not a credit decision or approval predictor.

| Readiness area | Ready | Needs attention | Not evaluated |

|---|---|---|---|

| Financial statements | |||

| YTD giving and operating trend | |||

| Reserves and available liquidity | |||

| Existing debt schedule | |||

| Repayment capacity | |||

| Board understanding and approval | |||

| Project scope and budget | |||

| Timeline and third-party requirements |

Print this page after completing the scorecard to capture your board's assessment for reference.

A Responsible Church-Financing Timeline

Actual timing varies. The sequence below is a planning framework, not a guaranteed duration.

Review the church's position, financing purpose, timing, and known gaps.

Organize statements, giving reports, debt schedules, budgets, board records, and explanations.

Confirm authority, approvals, scope, total cost, requested financing, and payment obligation.

Submit a complete and internally consistent application package.

The lender evaluates the transaction while appraisal, title, environmental, inspection, or construction requirements are completed as applicable.

Resolve conditions, finalize approvals, review closing documents, and complete authorization.

The loan closes, funds are disbursed, or the construction draw process begins.

Questions Church Leaders and Finance Committees Ask Most Often

Do church loans require a personal guarantee?

Requirements vary. Griffin almost never requires personal guarantees in church-loan transactions. Organizational strength, documentation, collateral, and transaction structure still matter.

How does a church know whether it is ready to apply?

It is not too early to contact Griffin while evaluating affordability or feasibility. A church is generally ready to submit a complete application when its records are reliable, the board understands and authorizes the obligation, the payment fits the budget, the purpose is sufficiently defined, and the timeline is orderly.

What financial documents are usually needed in the beginning?

A typical initial submission includes a completed Griffin application, three years of complete financial statements, current YTD financial statements, and a clear explanation of the proposed transaction. Additional information depends on the transaction.

How early should a church begin preparing?

Begin as early as practical — ideally several months before funds are needed. Construction and other complex transactions may require additional preparation time.

What does a lender evaluate in giving history?

Consistency, trajectory, seasonality, concentration, and whether monthly records reconcile with annual statements. A multi-year pattern provides more context than one isolated total.

Does the church board need to approve the loan?

Formal authorization is commonly required. The exact process depends on governing documents, legal structure, and the transaction.

Why are construction loans more complex?

Construction financing depends on a defined project, contractor, detailed budget, contingency, schedule, draw process, inspections, and completion or permanent-financing plan.

How is repayment capacity evaluated?

Debt-service coverage generally compares cash available for debt service with required annual debt payments. Lenders also consider existing obligations, reserve stability, operating trends, and transaction-specific adjustments.

What happens when a church is not yet ready?

The church can identify the most important gaps and create an action plan. An early conversation may still be useful; not every issue must be resolved before Griffin helps clarify the next responsible step.

How long can the process take?

There is no single universal timeline. It depends on loan type, file completeness, approvals, appraisal, title work, property or construction requirements, underwriting, and third-party conditions.

Church-Finance Expertise Since 1999

Griffin Church Loans supports churches considering property purchases, refinancing, renovations, expansions, and construction projects across the United States.

John Berardino, Founder and President

John Berardino leads Griffin Church Loans and has helped churches navigate financing decisions involving affordability, documentation, timing, governance, property, and construction. His published insights focus on practical preparation, responsible stewardship, and church-specific financing realities.

Founder profile · Case studies · Lessons from 2,000 church loans

Start With a Church Loan Readiness Conversation

A church does not need every answer before contacting Griffin. An initial conversation can clarify the church's current position, identify preparation gaps, and determine the most responsible next step.

Video transcript — A message from John Berardino

Hi, I'm John Berardino, President of Griffin Capital Funding, also known as Griffin Church Loans. We've been in business since 1999, and during that time we've closed more than 2,000 loans totaling over $2 billion for churches across the country. We finance church real estate for purchases, refinancing, renovations, and new construction.

Today I'd like to talk about church loans, how they work, what you can expect, and some of the common misconceptions people have about financing through Griffin Church Loans.

One of the most common concerns we hear is from pastors who have been told by their local bank that they or members of their congregation must personally guarantee a church loan. Many pastors understandably don't want to risk their personal assets or credit for a nonprofit organization.

At Griffin Church Loans, we almost never require personal guarantees. Once we review your church's financial information and determine that we can finance your project, we'll let you know upfront whether a personal guarantee is needed. In the overwhelming majority of cases, it isn't.

Another misconception involves construction loans. Many churches believe they should first hire an architect, pay for building plans, obtain third-party reports, and select a contractor before speaking with a lender.

We recommend doing exactly the opposite. Before spending money on plans, reports, or professional services, talk with us first. We'll review your financial statements at no cost and let you know how much your church is likely to qualify for. That gives you a realistic budget before you invest in architectural plans or other project expenses.

If you spend money on plans before knowing what financing is available, you may discover that the project exceeds your approved loan amount, requiring the plans to be redesigned and increasing your costs unnecessarily.

Again, I'm John Berardino, President of Griffin Church Loans. We invite you to contact us for a free consultation. We don't charge upfront fees, we'll analyze your financial statements, explain your financing options, and help you understand the best path forward. We've been serving thousands of churches for decades, and we'd love the opportunity to work with you. Thank you.

Fredericksburg, VA 22408

Griffin Church Loans Resources

Select any resource below to open it.

Independent Financial and Governance Resources

Educational Disclaimer: This brief is provided for general educational purposes only. It does not constitute a commitment to lend, an offer of financing, financial advice, legal advice, tax advice, or a statement of universal underwriting requirements. Loan availability, structure, documentation, timelines, and approval criteria vary by transaction, lender, loan type, property, project, and the financial condition of the borrowing church. All transactions are subject to review, underwriting, and approval.